Best Term Insurance Plans in UAE

Term insurance is an affordable and straightforward way to protect your loved ones financially in case something happens to you. It provides a lump sum payout to your beneficiaries if you pass away during the policy term, helping them cover expenses like bills, loans, or education.

4.6/5

27762

Insurance Partners

Trusted Customers

Policies Sold

PB Promise Best

PB Promise Best

Price Guarantee

In the UAE, term life plans are available with flexible terms and affordable premiums, making them accessible for anyone looking to secure their family's future. Explore the benefits of term insurance and choose the right plan to safeguard your loved ones today.

Best Term Insurance Plans in UAE

Some of the best Term Insurance quotes in UAE & Dubai are:

Term insurance is a pure life cover that financially secures life assured’s family in case the former passes away during the policy tenure. This type of life insurance is available only for a specific tenure.

Features of Term Insurance Plan

Here are some of the key features of term life insurance in the UAE -

- High Coverage at Low Cost – Get a large insured sum at affordable premiums

- Easy to Buy – Quick and simple application with minimal requirements — easily compare and purchase on Policybazaar.ae

- Flexible Payouts – Choose between a lump sum or staggered payments based on your needs

- Customisable Policy Term – Select a coverage period from 5 to 35 years, depending on your age and preference

- Flexible Premium Payments – Pay monthly, half-yearly, annually, or as a one-time lump sum

- Premium Waiver – If the insured becomes permanently disabled and is unable to work, premiums may be waived with an added rider

What are the Types of Term Insurance in the UAE?

Discussed below are the types of term insurance in the UAE —

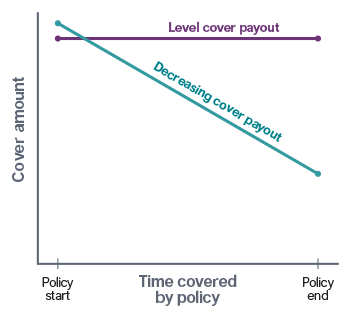

| Level Term Plans | Increasing Term Plans | Decreasing Term Plans | Convertible Term Plans |

|---|---|---|---|

| A basic plan where the coverage amount remains fixed throughout the policy — if the policyholder passes away, the nominee receives the full sum assured | The coverage amount increases every year while the premium remains the same — it offers more benefits compared to a Level Term Plan | Designed for those with loans, the coverage amount decreases over time as EMIs are paid, aligning with the reduced loan balance | Allows policyholders to switch to a different insurance type, such as whole life or endowment plans, if their needs change in the future |

Reasons to Buy a Term Insurance Plan

Listed below are the main reasons as to why a term plan is necessary in the UAE —

- Rising Liabilities – Many among us rely on loans rather than savings over time. With a term policy, your family can manage debts and daily expenses in your absence.

- Smaller Families, Bigger Risks – Unlike before, where extended families provided financial support, nuclear families face greater financial insecurity if a primary earner is lost.

- Growing Lifestyle Diseases – Health risks, especially for professionals in high-stress jobs, are increasing. This makes financial protection even more crucial.

- Impact of Inflation – Savings today may not be enough for future needs. With rising costs, a strong financial backup is necessary to secure your family’s future.

Best Term Insurance in the UAE 2025

Curated below is a list of some of the best term insurance plans in the UAE —

HAYAH Term Life Protect

|

Zurich International Term Assurance

|

MetLife Live Life

|

MetLife Live Life Now

|

Takaful Emarat Fixed Term

|

Sukoon DigiTermA pure term life insurance plan that provides financial protection to the nominee if the life assured passes away during the policy tenure.

|

LIC Life Protect Term Plan 278

|

|

Reasons to Buy a Term Insurance Plan

Listed below are the main reasons as to why a term plan is necessary in the UAE —

- Rising Liabilities – Many among us rely on loans rather than savings over time. With a term policy, your family can manage debts and daily expenses in your absence.

- Smaller Families, Bigger Risks – Unlike before, where extended families provided financial support, nuclear families face greater financial insecurity if a primary earner is lost.

- Growing Lifestyle Diseases – Health risks, especially for professionals in high-stress jobs, are increasing. This makes financial protection even more crucial.

- Impact of Inflation – Savings today may not be enough for future needs. With rising costs, a strong financial backup is necessary to secure your family’s future.

What are the Benefits of Term Plans?

Discussed below are the benefits of term insurance plans in the UAE -

| Affordable Premiums | Term plans offer high coverage at low costs. Premiums are based on age, meaning younger policyholders pay less. Payments can be made monthly, half-yearly, or annually. |

|---|---|

| Simple and Transparent | Term policies are straightforward, offering only life protection without any cash value. If the policyholder passes away, the full sum assured is paid to the nominee (usually a spouse or children). |

| Financial Security | This insurance type provides a strong financial safety net for dependents. This ensures their financial stability in the policyholder’s absence. |

| Flexible Options | In the UAE, you can find different plans catering to various needs. Types such as decreasing term insurance with lower premiums can be adjusted for family protection or loan repayment. |

| Essential Coverage | Term plans present a cost-effective option that offers necessary protection without unnecessary add-ons, keeping premiums reasonable. |

| Adequate Coverage | With a term life policy, you can get a high sum assured at nominal rates. |

Note: Experts suggest that the coverage should be at least 10 times your annual income.

Understanding the Difference Between Term Insurance and Whole Life Insurance

Here are the major differences between term insurance and whole life insurance in the UAE —

|

Term Life Insurance |

Whole Life Insurance |

|---|---|

| The policy tenure is pre-specified in the plan. |

Coverage for entire life |

|

There are no survival benefits; there is no payout if the life assured survives the policy tenure. |

The policy includes survival benefits and cash value that accumulates over time. |

|

More affordable premium and is suitable for individuals looking for cost-effective coverage. |

The premium is higher but fixed for the entire life. |

|

The death benefit is paid out if the life assured passes away during the policy tenure. |

There are two components available – death benefits and saving components. |

How Does Term Insurance Work in the UAE?

Here is an overview of how term insurance works in the UAE —

- Choosing the Policy - First, calculate how much coverage you need and for how long. Consider your financial commitments, like loans or education, when making this decision.

- Paying Premiums - Once you’ve selected the coverage and term, you’ll pay premiums to the insurer. These can be monthly, quarterly, or yearly, depending on your agreement.

- Death Benefit - If you pass away during the term, the insurance company will pay the agreed amount to your beneficiaries. This sum can cover debts, maintain the family’s lifestyle, or fund future needs like education or healthcare.

- No Payout if You Survive - If you live through the term, there is no payout — the policy ends unless you renew it. Some policies allow renewal without a medical exam, though premiums may rise with age.

- Policy Exclusions - Term insurance policies have exclusions, like death due to suicide within the first year or involvement in illegal activities. Be sure to understand these exclusions before buying a policy.

What are the Major Term Insurance Riders in the UAE?

Riders are optional add-ons that you can add to your term policy and get extra benefits beyond the basic coverage. Here are some common riders and their benefits —

- Critical Illness Rider - Provides a lump sum payout if the insured is diagnosed with a serious illness like cancer or a heart attack

- Terminal Illness Rider - Allows early access to part of the death benefit if diagnosed with a terminal illness

- Premium Waiver Rider - Waives future premium payments if the policyholder becomes disabled or unable to work

- Accidental Death Benefit Rider - Pays an extra amount if the death occurs due to an accident

- Permanent Total Disability Rider - Offers financial support if the insured becomes permanently disabled

- Second Medical Opinion Rider - Provides access to another specialist’s opinion for serious illnesses

- Temporary Life Cover Rider - Gives temporary coverage before the policy is officially issued

- Repatriation Benefit Rider - Covers the cost of transporting the insured’s remains back home if they pass away abroad

Which Factors Affect Your Term Insurance’s Premium?

Let’s understand the factors that impact your term life insurance’s premium —

- Age – Younger individuals pay lower premiums — a 25-year-old is likely to pay less than a 45-year-old due to lower health risk

- Health Condition – Good health means lower premiums — existing medical issues, on the other hand, can increase costs

- Coverage Amount – Higher coverage (e.g., AED 500,000 vs. AED 100,000) leads to higher premiums

- Policy Term – A 10-year policy is usually cheaper than a 30-year policy since longer coverage increases costs

- Smoking Status – Smokers pay more due to higher health risks

- Gender – Women often pay lower premiums due to their higher life expectancies

- Payment Frequency – Annual payments may be cheaper than monthly ones as some insurers offer discounts

Who Should Invest in Term Life Insurance in the UAE?

Term insurance is essential for working professionals, young parents, and those with dependent family members. It provides financial security for loved ones in case of unexpected events.

Let’s understand the importance of term insurance for individuals belonging to the following categories —

- Young Professionals – With fewer financial obligations, young professionals can secure high coverage at low premiums by starting early

- Parents – As primary earners, parents need term life insurance to ensure their family's financial security in case of any unfortunate event

- Newly Married Couples – A term plan provides financial support to a spouse, helping them manage expenses even in the policyholder’s absence

- Self-Employed Individuals – Entrepreneurs have financial responsibilities towards both their families and businesses — a term plan helps them protect both

- Working Women & Single Parents – A term policy ensures financial security for dependents, offering peace of mind in case of unforeseen circumstances

What are the Things to Keep in Mind When Buying a Term Insurance Plan?

To get the best coverage with your term plan, keep the following things in mind —

- Decide the Right Coverage Amount - Choose a plan that ensures your family can manage daily expenses in your absence. Consider both your income and your family's financial needs when selecting coverage.

- Consider Your Life Stage and Family Size - Financial responsibilities change over time. A single person has different needs than someone who is married or has children. Choose coverage that adapts to your life stage and growing responsibilities.

- Check the Claim Settlement Ratio - A higher claim settlement ratio means better chances of your family receiving the full sum assured. Choose an insurer with a strong track record of settling claims efficiently.

- Assess Your Family’s Needs - Select coverage that helps your family maintain their current lifestyle. Furthermore, factor in inflation and future expenses to ensure sufficient financial protection.

- Add Riders for Extra Protection - Enhance your coverage with riders like disability cover, premium waiver, or loss of employment cover for added security at a small extra cost.

- Include Outstanding Liabilities - If you have loans (home, car, or personal loans), add their repayment amount to your coverage to prevent the burden from falling on your family.

Where to Get Term Insurance in the UAE?

Getting the best term insurance in UAE is easy with Policybazaarinsurance.ae.

How to File Term Insurance Claims in the UAE?

Discussed below is the process to file a term insurance claim in the UAE —

- Notify the Insurance Company – Contact your insurer right away to inform them about the claim using the provided contact details

- Complete the Claim Form – Fill out the claim form carefully and make sure to provide all necessary information to avoid delays

- Submit the Claim – Submit the form and required documents through the insurer's preferred channels

- Provide Additional Information – If the insurer asks for more details or documents, provide them quickly to keep the process moving

- Claim Assessment – The insurer will review the claim, documents, and policy terms, and may investigate if needed

- Claim Settlement – Once approved, the insurer will pay the settlement amount as per your policy, via bank transfer or cheque

- Seek Assistance if Needed – If you need help or have any questions during the process, contact the insurer’s customer service or claims department

Note - Here is the list of the documents required to file a claim —

- Original policy document

- Death certificate (if the life assured passes away)

- Identification documents like Emirates ID

- Claim form (provided by the insurance provider)

- Medical records (if possible)

- Other supporting documents (as required by the insurance provider)

Glossary

| Plan Entry Age | The age when you start your insurance policy (e.g., if you buy at 30, your entry age is 30) |

|---|---|

| Policy Term | The duration your policy stays active (e.g., a 20-year policy lasts for 20 years) |

| Maturity | The time when your policy ends (e.g., a 20-year policy matures after 20 years) |

| Sum Assured | The guaranteed payout in case of death (e.g., AED 1,000,000) |

| Mode of Payment | How often you pay premiums (monthly, annually, and so on) |

| Ownership | The person who owns the policy (single life or joint life) |

| Beneficiary | The person who receives the payout if the insured passes away |

| Grace Period | Extra time after the due date to pay the premium without penalty or policy cancellation |

| Free Look Period | A short period (usually 30 days) to cancel the policy and get a refund |

| Reinstatement Period | The time allowed to restore a lapsed policy |

| Re-Insurer | A company that helps insurers manage risks by sharing them |

| Claim Settlement Ratio | The percentage of claims paid by the insurer (the higher the better) |

Frequently Asked Questions

Ideally, you should buy term insurance in the UAE in your early 20s to ensure a lower premium.

Your premium will only be refunded if you cancel your policy within the free-look period or if you choose the return of premium rider (if available). Otherwise, the premium is non-refundable

Term life insurance is a smart choice for anyone with a family to support. It gives you peace of mind, knowing your loved ones will be financially protected in case of unexpected events.

Usually, you cannot withdraw money from term life insurance — it's simply meant to provide a death benefit to your beneficiaries. However, some life policies might allow loans or partial surrenders in specific situations.

You can use term insurance calculators to determine the premiums in the UAE based on factors like your age, sum assured, and more.

More From Term Insurance

- Recents Articles

- Popular Articles

02 Jul 2025Difference Between Whole Life and Endowment Policy in UAECompare whole life vs endowment insurance in UAE. Understand their differences, benefits, and choose the right plan for your financial goals.

02 Jul 2025Difference Between Whole Life and Endowment Policy in UAECompare whole life vs endowment insurance in UAE. Understand their differences, benefits, and choose the right plan for your financial goals. 23 May 2025Expat Life Insurance in UAE: Best Plans & Complete GuideExplore everything about expat life insurance in the UAE – from top plans and benefits to key reasons why expats need coverage. Secure your family's future today.

23 May 2025Expat Life Insurance in UAE: Best Plans & Complete GuideExplore everything about expat life insurance in the UAE – from top plans and benefits to key reasons why expats need coverage. Secure your family's future today. 13 May 2025Universal Life Insurance in UAE: Benefits and TypesDiscover the advantages of Universal Life Insurance in the UAE. Learn about flexible premiums, investment options, types of UL policies, and how to build long-term wealth and protection.

13 May 2025Universal Life Insurance in UAE: Benefits and TypesDiscover the advantages of Universal Life Insurance in the UAE. Learn about flexible premiums, investment options, types of UL policies, and how to build long-term wealth and protection. 15 Apr 2025Term Insurance for Women in the UAEExplore affordable term insurance for women in the UAE. Learn about benefits, best plans, eligibility, and how to choose the right coverage to protect your family.

15 Apr 2025Term Insurance for Women in the UAEExplore affordable term insurance for women in the UAE. Learn about benefits, best plans, eligibility, and how to choose the right coverage to protect your family. 15 Apr 2025Life Insurance for Parents in UAELooking to secure your parents’ financial future? Explore life insurance for parents in the UAE, including benefits, types, how to apply, and what to consider when choosing a plan.

15 Apr 2025Life Insurance for Parents in UAELooking to secure your parents’ financial future? Explore life insurance for parents in the UAE, including benefits, types, how to apply, and what to consider when choosing a plan. 28 Feb 2025Best Term Insurance Plans for Self-Employed in UAE – Secure Your FutureExplore the best term insurance plans for self-employed individuals in the UAE. Get financial security for your family & business with affordable coverage options. Compare & apply now.

28 Feb 2025Best Term Insurance Plans for Self-Employed in UAE – Secure Your FutureExplore the best term insurance plans for self-employed individuals in the UAE. Get financial security for your family & business with affordable coverage options. Compare & apply now. 28 Feb 2025Zurich Futura Whole Life Insurance – Benefits, Features & Coverage in UAEDiscover Zurich Futura Whole Life Insurance in the UAE. Get lifelong coverage, flexible benefits, and investment growth. Learn about policy features, optional riders, and how to apply today!

28 Feb 2025Zurich Futura Whole Life Insurance – Benefits, Features & Coverage in UAEDiscover Zurich Futura Whole Life Insurance in the UAE. Get lifelong coverage, flexible benefits, and investment growth. Learn about policy features, optional riders, and how to apply today! 21 Feb 2025Best Life Insurance Companies in the UAE – Compare & Choose the Right PolicyLooking for the best life insurance companies in the UAE? Compare top insurers, coverage options, and claim settlement ratios to secure your family’s financial future.

21 Feb 2025Best Life Insurance Companies in the UAE – Compare & Choose the Right PolicyLooking for the best life insurance companies in the UAE? Compare top insurers, coverage options, and claim settlement ratios to secure your family’s financial future. 13 Feb 2025Term vs Whole Life Insurance in UAE: Key Differences & BenefitsCompare term and whole life insurance in the UAE. Understand key differences, benefits, costs, and which plan suits your financial goals and budget.

13 Feb 2025Term vs Whole Life Insurance in UAE: Key Differences & BenefitsCompare term and whole life insurance in the UAE. Understand key differences, benefits, costs, and which plan suits your financial goals and budget.- 11 Feb 2025Sum Insured vs Sum Assured: Key Differences & Insurance GuideUnderstand the difference between sum insured vs sum assured in insurance. Learn about their meanings, key features, and how to choose the right coverage for your needs.

23 Jul 2024Takaful Emarat Life Insurance | Choose Best Takaful Emarat Life Insurance in UAETakaful Emarat Life Insurance UAE - Compare & Buy Takaful Emarat Life Insurance in Dubai, UAE. Get Financial assurance for your family with a Takaful Emarat Life Insurance

23 Jul 2024Takaful Emarat Life Insurance | Choose Best Takaful Emarat Life Insurance in UAETakaful Emarat Life Insurance UAE - Compare & Buy Takaful Emarat Life Insurance in Dubai, UAE. Get Financial assurance for your family with a Takaful Emarat Life Insurance 15 May 2024Why Choose Twenty Five Year Term Life Insurance?In this article, we will understand all the key details about 25 year term insurance and its usefulness.

15 May 2024Why Choose Twenty Five Year Term Life Insurance?In this article, we will understand all the key details about 25 year term insurance and its usefulness. 15 May 2024Level or Decreasing Life Insurance: What's the Difference?In this article, we will explore the distinction between decreasing vs level insurance, the benefits of each type, and how you can determine what works best for you.

15 May 2024Level or Decreasing Life Insurance: What's the Difference?In this article, we will explore the distinction between decreasing vs level insurance, the benefits of each type, and how you can determine what works best for you. 16 May 2025Level Term Life Insurance in UAE – Features and BenefitsExplore Level Term Life Insurance in the UAE – enjoy fixed premiums, guaranteed death benefits, and flexible coverage terms. Ideal for affordable long-term protection.

16 May 2025Level Term Life Insurance in UAE – Features and BenefitsExplore Level Term Life Insurance in the UAE – enjoy fixed premiums, guaranteed death benefits, and flexible coverage terms. Ideal for affordable long-term protection.- 11 Mar 202410 Crore Life Insurance Policy - A Complete GuideA 10 crore life insurance policy offers extensive coverage. It ensures the financial well-being of the family and allows them to maintain their lifestyle and meet their financial goals even in the policyholder’s absence.

- 11 Mar 2024What is Surrender Value in Insurance?Surrender value in insurance is the amount of money a policyholder receives if they cancel their policy before it matures. Check two main types of surrender values - Guaranteed Surrender Value and Special Surrender Value.

- 11 Mar 2024Term Insurance Premium Calculator - A Complete GuideTerm insurance premium calculator in the UAE offers numerous advantages, streamlining the process of selecting the most suitable term insurance plan.

- 11 Mar 2024Term Insurance with Return of Premium - How Does It Work?Term insurance with return of premium – Learn about what this type of insurance is, how it works, and whether or not it’s right for you.

30 Jan 2024Who Should Be Your Nominee for Your Term Insurance?We will explore into the nuances of term insurance, elucidating the meaning of the insurance nominee meaning, life insurance nominee rules, and much more.

30 Jan 2024Who Should Be Your Nominee for Your Term Insurance?We will explore into the nuances of term insurance, elucidating the meaning of the insurance nominee meaning, life insurance nominee rules, and much more. 30 Jan 2024Understanding the Slide of Decreasing Term InsuranceWe will explore the nuances of the decreasing term life insurance plan, highlighting its salient features, benefits, and more.

30 Jan 2024Understanding the Slide of Decreasing Term InsuranceWe will explore the nuances of the decreasing term life insurance plan, highlighting its salient features, benefits, and more.

24 Jun 2025Term Insurance for NRIs in UAE: Best Plans in 2025Explore top term insurance plans for NRIs in the UAE. Secure your family's future with affordable coverage tailored for expatriates. Get a quote today!

24 Jun 2025Term Insurance for NRIs in UAE: Best Plans in 2025Explore top term insurance plans for NRIs in the UAE. Secure your family's future with affordable coverage tailored for expatriates. Get a quote today! 07 Aug 20231 Crore Term Insurance Plans In India: Here’s What You Need to Know!1 Crore Term Insurance Plans - Term insurance, a type of life insurance providing coverage for a specified tenure, offers a cost-effective way for individuals to financially protect their loved ones in the event of an unexpected death.

07 Aug 20231 Crore Term Insurance Plans In India: Here’s What You Need to Know!1 Crore Term Insurance Plans - Term insurance, a type of life insurance providing coverage for a specified tenure, offers a cost-effective way for individuals to financially protect their loved ones in the event of an unexpected death..png) 25 Apr 2025Best Life Insurance for Seniors | Protect Your FutureExplore affordable life insurance for seniors. Compare plans, get a quote, and find the best coverage for your needs. Start securing your future today!

25 Apr 2025Best Life Insurance for Seniors | Protect Your FutureExplore affordable life insurance for seniors. Compare plans, get a quote, and find the best coverage for your needs. Start securing your future today! 06 Dec 2024Life Insurance for Couples : Everything You Need to KnowMake sure your loved ones are taken care of – get life insurance for couples today! Explore the significance of life insurance for married couples and how it can provide a safety net for the family's financial well-being.

06 Dec 2024Life Insurance for Couples : Everything You Need to KnowMake sure your loved ones are taken care of – get life insurance for couples today! Explore the significance of life insurance for married couples and how it can provide a safety net for the family's financial well-being. 02 Aug 2023Understanding Life Insurance for 60 Year OldsLife insurance for senior citizens over 60 years numerous life insurance plans for coverage related to death, critical illnesses, situations where one is unable to work due to disabilities, and more.

02 Aug 2023Understanding Life Insurance for 60 Year OldsLife insurance for senior citizens over 60 years numerous life insurance plans for coverage related to death, critical illnesses, situations where one is unable to work due to disabilities, and more. 07 Aug 2023Term Life Insurance with Critical Illness CoverCritical illness covers a variety of illnesses, so be sure to find the right policy for you and your family. Check out our selection of term life insurance with critical illness cover today!

07 Aug 2023Term Life Insurance with Critical Illness CoverCritical illness covers a variety of illnesses, so be sure to find the right policy for you and your family. Check out our selection of term life insurance with critical illness cover today! 05 Sep 2023Your Ultimate Guide to Life Insurance Corporation of IndiaLife Insurance Corporation of India - LIC aims to serve as a comprehensive guide for all those interested in learning more about LIC of India, delving into the core aspects of the corporation, its offerings, and its impact on the lives of millions of Indians.

05 Sep 2023Your Ultimate Guide to Life Insurance Corporation of IndiaLife Insurance Corporation of India - LIC aims to serve as a comprehensive guide for all those interested in learning more about LIC of India, delving into the core aspects of the corporation, its offerings, and its impact on the lives of millions of Indians.- 14 Jun 2023Defining Spouse Term Insurance: Term Insurance for Husband and WifeWe will cover couple term insurance, discussing its importance, key features, benefits, and factors to consider when choosing a plan.

07 Aug 2023Life Insurance for 65 and Older - Benefits & TipsCheck out our top picks for 65+ life insurance plans! Learn more about the benefits of life insurance for those over 65 years old in this post.

07 Aug 2023Life Insurance for 65 and Older - Benefits & TipsCheck out our top picks for 65+ life insurance plans! Learn more about the benefits of life insurance for those over 65 years old in this post. 07 Aug 2023Life Insurance for Seniors over 70 Years - Benefits & TipsDon't wait until it's too late to get life insurance for seniors. Here are everything you need to know about getting life insurance for seniors over 70 years of age.

07 Aug 2023Life Insurance for Seniors over 70 Years - Benefits & TipsDon't wait until it's too late to get life insurance for seniors. Here are everything you need to know about getting life insurance for seniors over 70 years of age. 07 Aug 2023The Best Life Insurance Cover in the UAE - Securing Your Loved Ones' FutureLife Insurance Cover in UAE - We will show you the different types of life insurance available in the UAE and which is best for you.

07 Aug 2023The Best Life Insurance Cover in the UAE - Securing Your Loved Ones' FutureLife Insurance Cover in UAE - We will show you the different types of life insurance available in the UAE and which is best for you. 10 Jul 2023LIC Term Insurance 1 Crore – An OverviewWe will take a closer look at LIC term insurance 1 crore and cover all its related aspects.

10 Jul 2023LIC Term Insurance 1 Crore – An OverviewWe will take a closer look at LIC term insurance 1 crore and cover all its related aspects.- 07 Aug 2023Best Life Insurance for Seniors Over 75 in UAEExplore the importance of life insurance for seniors over 75, discuss the benefits it offers, and provide guidance on choosing the right policy. Get started today and find the best policy for you and your family!

02 Aug 2023Life Insurance For People Over 50 : Plans & BenefitsLife insurance also allows seniors to leave a legacy for their beneficiaries, offering a means to support their families or contribute to charitable causes.

02 Aug 2023Life Insurance For People Over 50 : Plans & BenefitsLife insurance also allows seniors to leave a legacy for their beneficiaries, offering a means to support their families or contribute to charitable causes. 24 Jun 2025Best Term Insurance Plan in India 2025Term insurance presents an economical way to secure one's family's financial future and have cover for their financial obligations such as mortgage payments, education expenses, and daily living costs.

24 Jun 2025Best Term Insurance Plan in India 2025Term insurance presents an economical way to secure one's family's financial future and have cover for their financial obligations such as mortgage payments, education expenses, and daily living costs. 02 Aug 2023How Many Types of Life Insurance Policies in UAEThere are different type fo policies in market like whole life, child life, and endowment life insurance policies, we intend to illuminate the unique characteristics and benefits of each type.

02 Aug 2023How Many Types of Life Insurance Policies in UAEThere are different type fo policies in market like whole life, child life, and endowment life insurance policies, we intend to illuminate the unique characteristics and benefits of each type.- 11 Mar 2024Term Insurance Premium Calculator - A Complete GuideTerm insurance premium calculator in the UAE offers numerous advantages, streamlining the process of selecting the most suitable term insurance plan.

- 06 Nov 2023Can You Have Two Life Insurance Policies?This article delves deep into the realm of holding multiple term insurance policies, highlighting the benefits and answering your pressing queries regarding this facet of financial planning.

02 Aug 2023Best 5 crore term life insurance: Best Term Plans in UAEWe will discuss 5 crore term life insurance in detail, whether it is suitable for you and your family, and other factors to keep in mind.

02 Aug 2023Best 5 crore term life insurance: Best Term Plans in UAEWe will discuss 5 crore term life insurance in detail, whether it is suitable for you and your family, and other factors to keep in mind. 02 Aug 2023Should I Buy Life Insurance in UAEExplores the different types of life insurance, the pros and cons of each one, and whether buying life insurance online in Dubai is a smart investment for your specific financial goals.

02 Aug 2023Should I Buy Life Insurance in UAEExplores the different types of life insurance, the pros and cons of each one, and whether buying life insurance online in Dubai is a smart investment for your specific financial goals.