Who Can Be a Nominee in Term Insurance, and Why Does It Matter?

You’ve done everything to secure your family’s future. You’ve bought a term insurance plan, carefully chosen the coverage, and paid premiums on time. But here’s something most people forget — choosing the right nominee.

4.6/5

35162

Insurance Partners

Trusted Customers

Policies Sold

PB Promise Best

PB Promise Best

Price Guarantee

A nominee in term insurance is not just a name on paper. This is the person who will receive the policy benefits if something unfortunate happens to you. The right nominee ensures that your hard-earned money reaches the right hands, quickly, safely, and without disputes.

What is a Nominee in Term Insurance?

A nominee in term insurance is the person you name in your policy. This individual will receive the death benefit if you pass away during the policy term. A nominee could be your spouse, child, parent, sibling, or even a trusted friend, depending on your personal situation.

The role of the nominee is crucial, as they are the one who gets financial coverage if you pass away. This ensures that the sum assured reaches your family without delay.

For instance, let’s assume a man named Ahmed names his wife Mahara as the nominee in his term insurance plan. In the unfortunate event of Ahmed’s death, she will receive the entire payout from the insurance company. This helps Mahara handle daily expenses, children’s education, or loan repayments — exactly as Ahmed would have wanted.

Best Term Insurance Plans in UAE

Some of the best Term Insurance quotes in UAE & Dubai are:

Importance of Nominee in Term Plan

Choosing a nominee is not just a formality — it’s a responsibility. Here’s why the importance of nominee in term plan cannot be overstated —

1. The Money Goes to the Right Person

When you choose a nominee, you are picking someone you trust — like your mom, dad, or brother — to get the money from your insurance. This makes sure it goes to the right person and doesn’t get lost or delayed.

2. Makes Things Faster and Easier

If the nominee’s name is already written in the policy, the insurance company can quickly give them the money. No extra waiting or confusion!

3. Reduces Conflicts

If you don’t choose a nominee, many people might end up in a dispute over who should get the money. Having a nominee keeps things peaceful and simple for your family.

4. Protects Your Family’s Financial Stability

Your term insurance nominee ensures your family continues to meet their needs: from school fees to loan EMIs, even when you’re no longer around.

Who Can Be a Nominee in Term Insurance?

Your life insurance policy allows you to nominate anyone with a legitimate connection to you. As per term insurance nominee rules, you can nominate anyone — family or non-family — as long as they meet certain eligibility criteria.

Let’s understand each category —

1. Spouse

Your husband or wife is the most common nominee choice. They are often the first in line to receive the death benefit since they manage household expenses and depend on your income.

2. Children

You can nominate one or more of your children. If they are minors (below 18 years), you must also appoint an appointee (a guardian) to manage the money until they become adults.

3. Parents

If you are unmarried or your parents depend on your income, nominating them ensures they remain financially secure.

4. Siblings

You may nominate a brother or sister if they are financially dependent on you. However, insurers may ask for proof of insurable interest.

5. Non-Family Members

In some cases, you can choose a close friend or distant relative as your nominee for term life insurance. However, this is usually allowed only if you can prove that the person has a valid financial dependency on you.

Types of Nominees in Term Insurance

When someone buys life coverage, they can choose who will get the money if something happens to them. These people are called nominees. Let’s look at the important type —

1. Beneficial Nominee

If you choose someone from your close family, like your mom, dad, husband, wife, or kids, they become beneficial nominees. This means only they will get the money from the insurance, even if someone else in the family asks for it. It’s a way to make sure your loved ones are taken care of first.

2. Minor Nominee

When your child is under 18, you can still name them as a nominee. However, you must also assign an appointee (guardian) to receive and manage the amount until your child turns 18.

3. Multiple Nominees

You can appoint more than one nominee and specify how much each will get. For instance, you can set 60% for your spouse and 40% for your child.

4. Contingent Nominee

This is your backup nominee. If your primary nominee cannot receive the payout, the contingent nominee will step in. It’s like having a safety net.

Term Insurance Nominee Rules You Should Know

Here are a few term insurance nominee rules that every policyholder should remember —

- You can change your nominee anytime during the policy term

- The latest nomination mentioned in the policy records is the one the insurer will honour

- If no nominee is mentioned, the insurance company will release the amount to your legal heirs

- Always keep the nominee’s details (age, address, relationship) updated with your insurer

- If your nominee is a minor, make sure to list a trustworthy appointee

Difference Between a Nominee and a Beneficiary

While many people use the terms ‘nominee’ and ‘beneficiary’ interchangeably, they serve different purposes. Let’s understand the differences in more detail —

| Aspect | Nominee | Beneficiary |

|---|---|---|

| Meaning | A person named to receive insurance benefits on behalf of the policyholder | The individual is legally entitled to inherit or utilise the benefits |

| Role | Acts as a custodian or trustee of the funds | Directly receives and uses the funds |

| Designation | Named in the insurance policy | Designated in wills, trusts, or legal documents |

| Applicability | Common for bank accounts, insurance, or property | Mostly applies to inheritance, wills, and trusts |

| Succession | Role doesn’t usually continue beyond initial receipt | Can include alternate beneficiaries for continuity |

What Happens If There’s No Nominee?

If you forget to nominate someone in your term insurance policy, the death benefit won’t automatically go to your family. Instead, your legal heirs will have to get a succession certificate or go through probate. The latter is a legal process that can delay access to funds.

In most cases, the amount is paid to your Class I legal heirs, which include —

- Spouse

- Children

- Parents

This delay can cause financial stress, which is why appointing a nominee is vital.

Can You Change Your Nominee in Term Insurance?

Yes, you can change or update your nominee at any time during the policy term. Life changes, marriages, children, divorces, or the passing of an existing nominee, make it essential to review and update this detail regularly.

All you need to do is submit a written request or online form to your insurer with the updated nominee details.

Things to Consider When Choosing a Nominee

Choosing the right nominee ensures your term insurance benefits reach the right person and serve their intended purpose. Here’s what to keep in mind —

| Factor | Why It Matters |

|---|---|

| Nominee’s Age | Minors need a guardian — adults can directly handle funds |

| Relationship | Ideally choose close family members who understand your dependents’ needs |

| Financial Dependence | Pick someone who truly depends on your income — like your spouse or children |

| Health | Select someone who is likely to outlive you and capable of managing long-term funds |

| Flexibility to Update | Be aware of how to modify nominees as your life circumstances change |

| Financial Awareness | Choose someone with basic financial understanding to manage proceeds wisely |

| Communication | Always inform your nominee and explain your expectations clearly |

| Estate Planning | Align your insurance nomination with your will or estate plan for consistency |

Mistakes to Avoid While Appointing a Nominee

Even a small mistake in choosing or managing your nominee details can create big problems for your family later.

Here are some common errors policyholders make and how you can avoid them —

1. Not informing the nominee

Your nominee should know that they are named in your term life insurance policy and where the relevant documents are stored. If the nominee is unaware, it could delay the claim process or worse, the benefits might remain unclaimed. Always share key details such as the policy number, insurer’s name, and claim process with them.

2. Not updating nominee details

Many policyholders forget to update their nominee information after such major events. This can cause legal complications during claim settlement. Regularly reviewing and updating your policy ensures the right person receives the benefit.

3. Choosing only one nominee

Relying on a single nominee is risky. In unfortunate cases where the primary nominee passes away before the policyholder or is unable to claim the benefit, the payout process becomes lengthy and complicated. Always appoint a contingent or secondary nominee — they can receive the claim amount if something happens to the first nominee.

4. Nominating a minor without an appointee

If your nominee is below the age of 18 years, you must legally appoint a guardian or appointee. This person will manage the insurance proceeds until the child becomes an adult.

Many people forget to do this. As a result, claim payouts get delayed or are held in court until a legal guardian is decided. To avoid such issues, always choose a responsible and trustworthy appointee.

5. Ignoring insurable interest

When nominating someone outside your family, such as a friend or distant relative, you must prove insurable interest. In plain terms, you need to prove that this person would face a financial loss if something happened to you. It’s safer to nominate family members or dependents unless you can legally establish this connection.

How to Choose the Right Nominee?

Choosing a nominee is like choosing a guardian for your family’s financial well-being. The right person will not only receive the money but will also manage it wisely to support your family’s future goals — whether it’s paying for a home loan, your child’s college fees, or everyday living expenses.

So, pick someone who is —

- Trustworthy

- Financially responsible

- Emotionally mature

- Capable of managing money well

Key Takeaways

- Always nominate someone in your life insurance plan, preferably a close family member

- You can name multiple or contingent nominees for extra security

- Review and update your nominee details after major life changes like marriage, childbirth, or divorce

- A beneficial nominee (spouse, children, parents) has the first legal right to claim the payout

- Without a nominee, your family may face long legal procedures to claim the benefits

Final Thoughts

A term life insurance policy is one of the most selfless investments you can make. But its true purpose is fulfilled only when your loved ones actually receive the benefits. That’s why the role of a term insurance nominee is so important.

Take a few minutes today to check your policy, review your nominee details, and make sure the person you trust most is listed correctly. Because when it comes to protecting your family’s future, every detail truly matters.

.jpg)

More From Term Insurance

- Recents Articles

- Popular Articles

29 May 2026Difference Between Life Insurance and Non-Life Insurance: Key Differences ExplainedUnderstand the difference between life and non-life insurance, including types, benefits, and key features. Learn how life vs general insurance works for UAE residents.

29 May 2026Difference Between Life Insurance and Non-Life Insurance: Key Differences ExplainedUnderstand the difference between life and non-life insurance, including types, benefits, and key features. Learn how life vs general insurance works for UAE residents. 13 Jan 2026Difference Between Insurance and Reinsurance: Meaning & Explained SimplyUnderstand the difference between insurance and reinsurance. Learn what reinsurance is, how it works, and why insurers in the UAE depend on it.

13 Jan 2026Difference Between Insurance and Reinsurance: Meaning & Explained SimplyUnderstand the difference between insurance and reinsurance. Learn what reinsurance is, how it works, and why insurers in the UAE depend on it.- 13 Jan 2026Term Insurance vs Permanent Insurance: Term Life vs Whole Life ExplainedTerm insurance vs permanent insurance explained. Compare term life vs whole life insurance, costs, benefits & see which is better for UAE residents and NRIs.

13 Jan 2026Home Loan Insurance vs Term Insurance: Which Is Better in the UAE?Home loan insurance vs term insurance explained for UAE home buyers. Compare cost, coverage & benefits to see which insurance is better for home loan protection.

13 Jan 2026Home Loan Insurance vs Term Insurance: Which Is Better in the UAE?Home loan insurance vs term insurance explained for UAE home buyers. Compare cost, coverage & benefits to see which insurance is better for home loan protection..jpg) 03 Sep 2025Expat Life Insurance in Dubai & UAE – Best Plans, Benefits & GuideLooking for expat life insurance in Dubai or UAE? Compare top providers like MetLife, Zurich, HAYAH & Sukoon. Learn eligibility, benefits, costs, and how life cover protects your family abroad.

03 Sep 2025Expat Life Insurance in Dubai & UAE – Best Plans, Benefits & GuideLooking for expat life insurance in Dubai or UAE? Compare top providers like MetLife, Zurich, HAYAH & Sukoon. Learn eligibility, benefits, costs, and how life cover protects your family abroad. 03 Sep 2025Medical Test for Life Insurance in UAE – Requirements, Process & BenefitsLearn when a medical test is required for life insurance in the UAE. Check the list of common medical exams, eligibility rules, and how tests impact premiums and claim approvals.

03 Sep 2025Medical Test for Life Insurance in UAE – Requirements, Process & BenefitsLearn when a medical test is required for life insurance in the UAE. Check the list of common medical exams, eligibility rules, and how tests impact premiums and claim approvals. 02 Jul 2025Difference Between Whole Life and Endowment Policy in UAECompare whole life vs endowment insurance in UAE. Understand their differences, benefits, and choose the right plan for your financial goals.

02 Jul 2025Difference Between Whole Life and Endowment Policy in UAECompare whole life vs endowment insurance in UAE. Understand their differences, benefits, and choose the right plan for your financial goals. 23 May 2025Expat Life Insurance in UAE: Best Plans & Complete GuideExplore everything about expat life insurance in the UAE – from top plans and benefits to key reasons why expats need coverage. Secure your family's future today.

23 May 2025Expat Life Insurance in UAE: Best Plans & Complete GuideExplore everything about expat life insurance in the UAE – from top plans and benefits to key reasons why expats need coverage. Secure your family's future today. 30 Oct 2025Universal Life Insurance in UAE: Benefits and TypesDiscover the advantages of Universal Life Insurance in the UAE. Learn about flexible premiums, investment options, types of UL policies, and how to build long-term wealth and protection.

30 Oct 2025Universal Life Insurance in UAE: Benefits and TypesDiscover the advantages of Universal Life Insurance in the UAE. Learn about flexible premiums, investment options, types of UL policies, and how to build long-term wealth and protection. 15 Apr 2025Term Insurance for Women in the UAEExplore affordable term insurance for women in the UAE. Learn about benefits, best plans, eligibility, and how to choose the right coverage to protect your family.

15 Apr 2025Term Insurance for Women in the UAEExplore affordable term insurance for women in the UAE. Learn about benefits, best plans, eligibility, and how to choose the right coverage to protect your family. 15 Apr 2025Life Insurance for Parents in UAELooking to secure your parents’ financial future? Explore life insurance for parents in the UAE, including benefits, types, how to apply, and what to consider when choosing a plan.

15 Apr 2025Life Insurance for Parents in UAELooking to secure your parents’ financial future? Explore life insurance for parents in the UAE, including benefits, types, how to apply, and what to consider when choosing a plan. 28 Feb 2025Best Term Insurance Plans for Self-Employed in UAE – Secure Your FutureExplore the best term insurance plans for self-employed individuals in the UAE. Get financial security for your family & business with affordable coverage options. Compare & apply now.

28 Feb 2025Best Term Insurance Plans for Self-Employed in UAE – Secure Your FutureExplore the best term insurance plans for self-employed individuals in the UAE. Get financial security for your family & business with affordable coverage options. Compare & apply now. 28 Feb 2025Zurich Futura Whole Life Insurance – Benefits, Features & Coverage in UAEDiscover Zurich Futura Whole Life Insurance in the UAE. Get lifelong coverage, flexible benefits, and investment growth. Learn about policy features, optional riders, and how to apply today!

28 Feb 2025Zurich Futura Whole Life Insurance – Benefits, Features & Coverage in UAEDiscover Zurich Futura Whole Life Insurance in the UAE. Get lifelong coverage, flexible benefits, and investment growth. Learn about policy features, optional riders, and how to apply today! 21 Feb 2025Best Life Insurance Companies in the UAE – Compare & Choose the Right PolicyLooking for the best life insurance companies in the UAE? Compare top insurers, coverage options, and claim settlement ratios to secure your family’s financial future.

21 Feb 2025Best Life Insurance Companies in the UAE – Compare & Choose the Right PolicyLooking for the best life insurance companies in the UAE? Compare top insurers, coverage options, and claim settlement ratios to secure your family’s financial future. 19 Aug 2025Term vs Whole Life Insurance in UAE: Key Differences & BenefitsCompare term and whole life insurance in the UAE. Understand key differences, benefits, costs, and which plan suits your financial goals and budget.

19 Aug 2025Term vs Whole Life Insurance in UAE: Key Differences & BenefitsCompare term and whole life insurance in the UAE. Understand key differences, benefits, costs, and which plan suits your financial goals and budget.- 11 Feb 2025Sum Insured vs Sum Assured: Key Differences & Insurance GuideUnderstand the difference between sum insured vs sum assured in insurance. Learn about their meanings, key features, and how to choose the right coverage for your needs.

23 Jul 2024Takaful Emarat Life Insurance | Choose Best Takaful Emarat Life Insurance in UAETakaful Emarat Life Insurance UAE - Compare & Buy Takaful Emarat Life Insurance in Dubai, UAE. Get Financial assurance for your family with a Takaful Emarat Life Insurance

23 Jul 2024Takaful Emarat Life Insurance | Choose Best Takaful Emarat Life Insurance in UAETakaful Emarat Life Insurance UAE - Compare & Buy Takaful Emarat Life Insurance in Dubai, UAE. Get Financial assurance for your family with a Takaful Emarat Life Insurance 15 May 2024Why Choose Twenty Five Year Term Life Insurance?In this article, we will understand all the key details about 25 year term insurance and its usefulness.

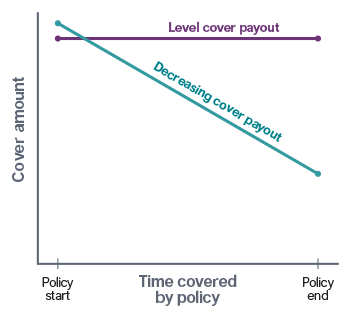

15 May 2024Why Choose Twenty Five Year Term Life Insurance?In this article, we will understand all the key details about 25 year term insurance and its usefulness. 15 May 2024Level or Decreasing Life Insurance: What's the Difference?In this article, we will explore the distinction between decreasing vs level insurance, the benefits of each type, and how you can determine what works best for you.

15 May 2024Level or Decreasing Life Insurance: What's the Difference?In this article, we will explore the distinction between decreasing vs level insurance, the benefits of each type, and how you can determine what works best for you. 16 May 2025Level Term Life Insurance in UAE – Features and BenefitsExplore Level Term Life Insurance in the UAE – enjoy fixed premiums, guaranteed death benefits, and flexible coverage terms. Ideal for affordable long-term protection.

16 May 2025Level Term Life Insurance in UAE – Features and BenefitsExplore Level Term Life Insurance in the UAE – enjoy fixed premiums, guaranteed death benefits, and flexible coverage terms. Ideal for affordable long-term protection.

23 Oct 2025Term Insurance for NRIs in UAE: Best Plans in 2026Explore top term insurance plans for NRIs in the UAE. Secure your family's future with affordable coverage tailored for expatriates. Get a quote today!

23 Oct 2025Term Insurance for NRIs in UAE: Best Plans in 2026Explore top term insurance plans for NRIs in the UAE. Secure your family's future with affordable coverage tailored for expatriates. Get a quote today!.png) 25 Apr 2025Best Life Insurance for Seniors | Protect Your FutureExplore affordable life insurance for seniors. Compare plans, get a quote, and find the best coverage for your needs. Start securing your future today!

25 Apr 2025Best Life Insurance for Seniors | Protect Your FutureExplore affordable life insurance for seniors. Compare plans, get a quote, and find the best coverage for your needs. Start securing your future today! 07 Aug 20231 Crore Term Insurance Plans In India: Here’s What You Need to Know!1 Crore Term Insurance Plans - Term insurance, a type of life insurance providing coverage for a specified tenure, offers a cost-effective way for individuals to financially protect their loved ones in the event of an unexpected death.

07 Aug 20231 Crore Term Insurance Plans In India: Here’s What You Need to Know!1 Crore Term Insurance Plans - Term insurance, a type of life insurance providing coverage for a specified tenure, offers a cost-effective way for individuals to financially protect their loved ones in the event of an unexpected death. 06 Dec 2024Life Insurance for Couples : Everything You Need to KnowMake sure your loved ones are taken care of – get life insurance for couples today! Explore the significance of life insurance for married couples and how it can provide a safety net for the family's financial well-being.

06 Dec 2024Life Insurance for Couples : Everything You Need to KnowMake sure your loved ones are taken care of – get life insurance for couples today! Explore the significance of life insurance for married couples and how it can provide a safety net for the family's financial well-being. 02 Aug 2023Understanding Life Insurance for 60 Year OldsLife insurance for senior citizens over 60 years numerous life insurance plans for coverage related to death, critical illnesses, situations where one is unable to work due to disabilities, and more.

02 Aug 2023Understanding Life Insurance for 60 Year OldsLife insurance for senior citizens over 60 years numerous life insurance plans for coverage related to death, critical illnesses, situations where one is unable to work due to disabilities, and more. 07 Aug 2023Term Life Insurance with Critical Illness CoverCritical illness covers a variety of illnesses, so be sure to find the right policy for you and your family. Check out our selection of term life insurance with critical illness cover today!

07 Aug 2023Term Life Insurance with Critical Illness CoverCritical illness covers a variety of illnesses, so be sure to find the right policy for you and your family. Check out our selection of term life insurance with critical illness cover today! 05 Sep 2023Your Ultimate Guide to Life Insurance Corporation of IndiaLife Insurance Corporation of India - LIC aims to serve as a comprehensive guide for all those interested in learning more about LIC of India, delving into the core aspects of the corporation, its offerings, and its impact on the lives of millions of Indians.

05 Sep 2023Your Ultimate Guide to Life Insurance Corporation of IndiaLife Insurance Corporation of India - LIC aims to serve as a comprehensive guide for all those interested in learning more about LIC of India, delving into the core aspects of the corporation, its offerings, and its impact on the lives of millions of Indians.- 23 Sep 2025Defining Spouse Term Insurance: Term Insurance for Husband and WifeWe will cover couple term insurance, discussing its importance, key features, benefits, and factors to consider when choosing a plan.

24 Jun 2025Best Term Insurance Plan in India 2026Term insurance presents an economical way to secure one's family's financial future and have cover for their financial obligations such as mortgage payments, education expenses, and daily living costs.

24 Jun 2025Best Term Insurance Plan in India 2026Term insurance presents an economical way to secure one's family's financial future and have cover for their financial obligations such as mortgage payments, education expenses, and daily living costs. 07 Aug 2023Life Insurance for 65 and Older - Benefits & TipsCheck out our top picks for 65+ life insurance plans! Learn more about the benefits of life insurance for those over 65 years old in this post.

07 Aug 2023Life Insurance for 65 and Older - Benefits & TipsCheck out our top picks for 65+ life insurance plans! Learn more about the benefits of life insurance for those over 65 years old in this post.- 09 Dec 2025Term Insurance Premium Calculator - A Complete GuideTerm insurance premium calculator in the UAE offers numerous advantages, streamlining the process of selecting the most suitable term insurance plan.

19 Sep 2025LIC Term Insurance 1 Crore – An OverviewWe will take a closer look at LIC term insurance 1 crore and cover all its related aspects.

19 Sep 2025LIC Term Insurance 1 Crore – An OverviewWe will take a closer look at LIC term insurance 1 crore and cover all its related aspects. 07 Aug 2023The Best Life Insurance Cover in the UAE - Securing Your Loved Ones' FutureLife Insurance Cover in UAE - We will show you the different types of life insurance available in the UAE and which is best for you.

07 Aug 2023The Best Life Insurance Cover in the UAE - Securing Your Loved Ones' FutureLife Insurance Cover in UAE - We will show you the different types of life insurance available in the UAE and which is best for you. 07 Aug 2023Life Insurance for Seniors over 70 Years - Benefits & TipsDon't wait until it's too late to get life insurance for seniors. Here are everything you need to know about getting life insurance for seniors over 70 years of age.

07 Aug 2023Life Insurance for Seniors over 70 Years - Benefits & TipsDon't wait until it's too late to get life insurance for seniors. Here are everything you need to know about getting life insurance for seniors over 70 years of age. 02 Aug 2023Best 5 crore term life insurance: Best Term Plans in UAEWe will discuss 5 crore term life insurance in detail, whether it is suitable for you and your family, and other factors to keep in mind.

02 Aug 2023Best 5 crore term life insurance: Best Term Plans in UAEWe will discuss 5 crore term life insurance in detail, whether it is suitable for you and your family, and other factors to keep in mind.- 06 Nov 2023Can You Have Two Life Insurance Policies?This article delves deep into the realm of holding multiple term insurance policies, highlighting the benefits and answering your pressing queries regarding this facet of financial planning.

02 Aug 2023Life Insurance For People Over 50 : Plans & BenefitsLife insurance also allows seniors to leave a legacy for their beneficiaries, offering a means to support their families or contribute to charitable causes.

02 Aug 2023Life Insurance For People Over 50 : Plans & BenefitsLife insurance also allows seniors to leave a legacy for their beneficiaries, offering a means to support their families or contribute to charitable causes. 30 Oct 2025How Many Types of Life Insurance Policies in UAEThere are different type fo policies in market like whole life, child life, and endowment life insurance policies, we intend to illuminate the unique characteristics and benefits of each type.

30 Oct 2025How Many Types of Life Insurance Policies in UAEThere are different type fo policies in market like whole life, child life, and endowment life insurance policies, we intend to illuminate the unique characteristics and benefits of each type. 03 Jan 2024Life Insurance for Young Adults - Securing Your Tomorrow, Today!We will explore the significance of life insurance for young adults, the various options available, and why it's a wise decision to secure your future today.

03 Jan 2024Life Insurance for Young Adults - Securing Your Tomorrow, Today!We will explore the significance of life insurance for young adults, the various options available, and why it's a wise decision to secure your future today.- 07 Aug 2023Best Life Insurance for Seniors Over 75 in UAEExplore the importance of life insurance for seniors over 75, discuss the benefits it offers, and provide guidance on choosing the right policy. Get started today and find the best policy for you and your family!