Best Term Insurance Plans in UAE

Term insurance is an affordable and straightforward way to protect your loved ones financially in case something happens to you. It provides a lump sum payout to your beneficiaries if you pass away during the policy term, helping them cover expenses like bills, loans, or education.

4.6/5

34393

Insurance Partners

Trusted Customers

Policies Sold

PB Promise Best

PB Promise Best

Price Guarantee

Term Insurance is a pure protection plan. It provides coverage for a fixed period, usually between 5 to 35 years. You pay a fixed premium for a certain number of years (the “term”), and if you pass away during that period, your family receives a payout (sum assured).

Unlike whole life or ULIP plans, term insurance in UAE does not have an investment component, making it budget-friendly while offering high coverage.

Example: If you buy a 20-year term plan in Dubai with AED 1 million coverage and pay AED 50/month, your family gets the AED 1 million payout if you pass away within those 20 years.

Best Term Insurance Plans in UAE

Some of the best Term Insurance quotes in UAE & Dubai are:

Why Should You Buy Term Life Insurance UAE?

Living in the UAE comes with its own financial responsibilities — from rising rent and mortgages to loans, education expenses, and high medical costs. If the main earning member is no longer around, a family can struggle to manage itself. Term life insurance in UAE makes sure that doesn’t happen.

Here’s why people choose it —

- Future Security for Children → Education in the UAE is expensive. A term policy guarantees that your kids’ future is secure.

- Homes are Getting Costly → Rents and property prices continue to rise. Term cover ensures your family can afford rent, housing, and daily expenses.

- Most People Have Loans → From car loans to mortgages, debts are common. You can use term insurance money to pay off outstanding mortgages, car loans, or personal loans.

- Healthcare Costs are High → Even young professionals are facing lifestyle diseases. The best term insurance plan covers sudden health-related deaths or critical illnesses.

- Expats Need Protection → There are not many long-term social security or government benefits for expats’ families in the UAE yet. Term insurance fills this gap.

Types of Term Insurance Plans in the UAE

Not all term insurance plans are the same. Here are the main types available —

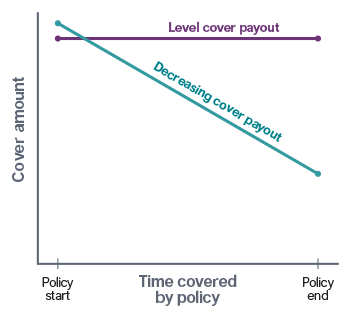

1. Level Term Insurance: ;

The cover amount stays the same throughout the policy term. It is ideal if you want fixed protection for family expenses, education, or long-term security.

Example: AED 1 million cover today will still be AED 1 million in year 25.

2. Increasing Term Insurance: ;

The cover increases each year, usually to match inflation or rising financial responsibilities. This term insurance plan is perfect if you expect your family’s needs to grow, like children’s education or rising living costs in Dubai.

Example: AED 1 million cover today could become AED 1.2 million in 5 years.

3. Decreasing Term Insurance: ;

The cover amount reduces every year on a pre-set basis. It’s great for covering loans (like mortgages) that shrink over time.

Example: If your home loan is AED 800,000 today but will reduce each year, your term insurance cover will also reduce accordingly.

5 Best Term Life Insurance in UAE 2026

To help you choose the best term life insurance in UAE, we’ve shortlisted some of the most trusted term insurance providers with their plan details, coverage, riders, and costs.

The plans mentioned below are for a 30-year-old male, a non-smoker, looking for AED 1M coverage in 30-year tenure. You can add your details to get a customised quote.

Sukoon Family Takaful TermClaim Settlement Ratio: 99% Key Features

|

MetLife Live Life NowClaim Settlement Ratio: 98.1% Key Features

|

Sukoon Life GuardClaim Settlement Ratio: 97.5% Key Features

|

MetLife Live Life Now

Claim Settlement Ratio: 98% Key Features

|

Zurich International Term AssuranceClaim Settlement Ratio: 98% Key Features

|

|

How to Choose the Best Term Life Insurance in UAE?

Here’s what you should keep in mind while picking the best term insurance plan for yourself and your family —

Pick the Right Type of Policy

The type of policy you choose should match your financial goals and lifestyle.

- Uniform cover → Level Term

- Rising expenses → Increasing Term

- Loans/mortgages → Decreasing Term

Consider current financial situation and your prospects. That way, you’ll know which type of cover is most suitable.

Choose the Right Sum Assured

Experts recommend coverage worth 10 to 15 times your annual income. Therefore, if you earn AED 200,000 a year, you should look at a policy worth AED 2–3 million. Use online term insurance calculators to figure out exactly how much cover you need, based on your lifestyle, debts, and family expenses.

- Add Optional Riders for Extra Protection

Basic term insurance covers death, but you can make your policy stronger by adding riders. These are additional coverage that give you extra benefits — - Accidental Death Benefit Rider → If you pass away in an accident, your family gets an additional payout on top of the basic cover.

- Critical Illness Rider → If you are diagnosed with a major illness, you’ll get a lump sum while you’re alive. This helps with hospital bills or income replacement. This rider can be accelerated or a standalone policy.

- Waiver of Premium Rider → If you become permanently disabled or critically ill and can’t work, your insurer waives all future premiums, keeping your policy active without any payments from your side.

Check Claim Settlement Ratio (CSR)

A CSR of 94–98% (as seen with top UAE insurers) means almost all claims get paid out without hassle. This figure is publicly available, so always compare insurers before making a decision.

Balance Between Premium and Coverage

It’s natural to look for the cheapest plan, but cheapest isn’t always the best. You should focus on a balance between affordable premiums and comprehensive coverage. Check if the premium is sustainable for you in the long run (since term insurance is usually for 20–30 years).

If you’re wondering, “How much premium do I pay for my term life insurance in Dubai?” The answer depends on your age, income, health, and lifestyle.

A term insurance calculator makes this easy. You just enter details like your:

- Age and date of birth

- Monthly income

- Smoking/non-smoking status

- Desired cover amount and policy tenure

The tool then shows your approximate premium and suggests the best term insurance plan in UAE based on your profile.

You can use Term Insurance Calculator from Policybazaarinsurance.ae, an online tool, to estimate the amount you would need to pay for free.

Benefits of Purchasing Term Life Insurance in UAE

Over 88% of UAE residents are expats. Most live away from their extended families and rely on their own income. A significant advantage is that most UAE term life insurance policies provide global coverage. Even if you relocate to another country for work or retirement, your protection remains active.

One of the most attractive features is affordability. Example: A healthy 30-year-old non-smoker in Dubai can receive AED 1 million cover starting at less than AED 100 per month.

You can choose a short cover of just 5 years, or long-term protection up to 35 years, depending on whether you want to cover short debts (like a car loan) or long-term responsibilities (like your child’s education).

The application process is quick and requires minimal documentation. In many cases, online applications are approved instantly, and medical tests may only be required for higher coverage amounts.

Who Should Buy Term Insurance in Dubai, UAE?

Everyone can benefit from term life insurance in Dubai, UAE, but the reasons may vary depending on your life stage. Here’s how it applies to you —

- Young Professionals: If you’re just starting your career in Dubai, buying term insurance early means you lock in much cheaper premiums for life.

- Parents: With term life insurance, you create a financial cushion that covers school fees, rent, household expenses, and even long-term savings goals such as university education.

- Newly Married Couples: Marriage brings new responsibilities, shared rent or mortgage, joint loans, and plans for the future. A term plan helps you make sure your partner is protected, debts are cleared, and your shared financial goals aren’t derailed.

- Self-Employed Individuals: If you run your own business or freelance in Dubai, you don’t get the employer-provided life cover that salaried people often enjoy. That makes buying your own term life insurance even more critical.

- Single Mothers & Working Women: If you are the sole breadwinner, your children rely completely on your income. Term insurance gives you peace of mind that, no matter what happens, your needs, from school to living expenses, are always secured.

Payout Options for Term Insurance in UAE

When it comes to paying the death benefit, insurers in Dubai give you flexibility to choose how your family will receive the money —

One-time Lump-sum Payout: Your family receives the entire benefit at once. This is useful for clearing loans, mortgages, or other large debts immediately.

Quick Comparison: Term Insurance vs Life Insurance

Here’s a brief comparison between term and life insurance to help you identify the suitable one for you —

| Parameter | Term Insurance | Life Insurance |

|---|---|---|

| Tenure | 5–35 years | Whole life |

| Benefits | Death benefit only | Death + maturity benefits |

| Premium | Very low | Higher |

| Cash Value | No cash value | Builds cash value |

| Best For | Affordable, pure protection | Insurance + investment |

If you want a more detailed comparison, read our article on the Difference between term insurance and life insurance.

Where to Get Term Insurance in the UAE?

Buying term life insurance in Dubai or anywhere in the UAE is now simpler than ever, thanks to online platforms like Policybazaarinsurance.ae.

Here’s how you can do it —

- Head to the website and select “Term Insurance” from the top menu

- Enter your basic information, like your name, age, phone number, and annual income

- Click on “View Quotes” and within seconds, you’ll see the best term life insurance options in the UAE

- Compare coverage, benefits, riders, claim settlement ratio, and premium costs—all in one place

- Click “Apply” and follow the guided steps, and upload the required documents

With Policybazaarinsurance.ae, you stay in control, choosing the right plan at the right cost without pressure or confusion.

- No hidden fees

- 100% online convenience

- Multiple insurer options in one place

How to File Term Insurance Claims in the UAE?

Filing a term insurance claim in the UAE is a straightforward process, provided you follow all the steps and keep documents ready. Here’s how it works —

Notify the Insurance Company: Most companies provide a dedicated claims helpline, email ID, or online portal. Quick notification helps start the claim process without delays.

Complete the Claim Form: Download or request the insurer’s claim form. Fill it carefully with accurate details about the policy.

Submit the Claim with Documents: Attach all required documents and submit them via the insurer’s preferred channel: online upload, email, or physical branch submission.

Provide Additional Information if Required: Sometimes, insurers may ask for extra documents or clarifications, such as hospital records, police reports (in case of accidental death), or additional ID proofs. Submit these promptly to avoid delays.

Claim Assessment & Settlement: The insurance company will review the claim. Once everything is verified, the insurer will release the payout to the nominee/beneficiary. The settlement is usually done via bank transfer or cheque.

Documents Required to Buy Term Life Insurance in UAE

Whether you’re a UAE national, resident, or expat, insurers will ask for some basic documents —

- UAE Nationals/Residents: Emirates ID

- Expats: Valid Passport + Emirates ID

- Proof of Address: Utility bills or rental agreement

Pro Tip: Always keep a copy of the policy documents, nominee details, and key insurer contact numbers handy. This helps your family file a claim faster in case of emergency.

Glossary

| Plan Entry Age | The age when you start your insurance policy (e.g., if you buy at 30, your entry age is 30) |

|---|---|

| Policy Term | The duration your policy stays active (e.g., a 20-year policy lasts for 20 years) |

| Maturity | The time when your policy ends (e.g., a 20-year policy matures after 20 years) |

| Sum Assured | The guaranteed payout in case of death (e.g., AED 1,000,000) |

| Mode of Payment | How often you pay premiums (monthly, annually, and so on) |

| Ownership | The person who owns the policy (single life or joint life) |

| Beneficiary | The person who receives the payout if the insured passes away |

| Grace Period | Extra time after the due date to pay the premium without penalty or policy cancellation |

| Free Look Period | A short period (usually 30 days) to cancel the policy and get a refund |

| Reinstatement Period | The time allowed to restore a lapsed policy |

| Re-Insurer | A company that helps insurers manage risks by sharing them |

| Claim Settlement Ratio | The percentage of claims paid by the insurer (the higher the better) |

Frequently Asked Questions

What is the best age to buy term insurance in the UAE?

It’s best to buy a term insurance plan in the UAE in your 20s or early 30s. You’ll lock in much lower premiums when you’re young and healthy.

Is term insurance refundable?

A term insurance policy in the UAE is non-refundable. You only get your money back if you cancel within the free-look period.

Why should you buy a term insurance policy?

Buying term life insurance in Dubai, UAE, ensures that your family is financially secure if something happens to you. It covers significant expenses such as loans, education, or day-to-day living costs.

Can you withdraw money from your term insurance in the UAE?

No, you usually can’t withdraw money from a term insurance plan in the UAE, as it’s meant only to pay your family a death benefit. Some other life insurance policies may allow partial withdrawals or loans.

How can you calculate term insurance premiums in the UAE?

You can check the cost of a term insurance using an online premium calculator. Simply enter your age, coverage amount, and other details to get an estimate.

Can NRIs buy term insurance in India?

Yes, if you’re an NRI living in the UAE, experts advise that you should buy term insurance in the UAE for better coverage.

More From Term Insurance

- Recents Articles

- Popular Articles

13 Jan 2026Difference Between Insurance and Reinsurance: Meaning & Explained SimplyUnderstand the difference between insurance and reinsurance. Learn what reinsurance is, how it works, and why insurers in the UAE depend on it.

13 Jan 2026Difference Between Insurance and Reinsurance: Meaning & Explained SimplyUnderstand the difference between insurance and reinsurance. Learn what reinsurance is, how it works, and why insurers in the UAE depend on it.- 13 Jan 2026Term Insurance vs Permanent Insurance: Term Life vs Whole Life ExplainedTerm insurance vs permanent insurance explained. Compare term life vs whole life insurance, costs, benefits & see which is better for UAE residents and NRIs.

13 Jan 2026Home Loan Insurance vs Term Insurance: Which Is Better in the UAE?Home loan insurance vs term insurance explained for UAE home buyers. Compare cost, coverage & benefits to see which insurance is better for home loan protection.

13 Jan 2026Home Loan Insurance vs Term Insurance: Which Is Better in the UAE?Home loan insurance vs term insurance explained for UAE home buyers. Compare cost, coverage & benefits to see which insurance is better for home loan protection..jpg) 03 Sep 2025Expat Life Insurance in Dubai & UAE – Best Plans, Benefits & GuideLooking for expat life insurance in Dubai or UAE? Compare top providers like MetLife, Zurich, HAYAH & Sukoon. Learn eligibility, benefits, costs, and how life cover protects your family abroad.

03 Sep 2025Expat Life Insurance in Dubai & UAE – Best Plans, Benefits & GuideLooking for expat life insurance in Dubai or UAE? Compare top providers like MetLife, Zurich, HAYAH & Sukoon. Learn eligibility, benefits, costs, and how life cover protects your family abroad. 03 Sep 2025Medical Test for Life Insurance in UAE – Requirements, Process & BenefitsLearn when a medical test is required for life insurance in the UAE. Check the list of common medical exams, eligibility rules, and how tests impact premiums and claim approvals.

03 Sep 2025Medical Test for Life Insurance in UAE – Requirements, Process & BenefitsLearn when a medical test is required for life insurance in the UAE. Check the list of common medical exams, eligibility rules, and how tests impact premiums and claim approvals. 02 Jul 2025Difference Between Whole Life and Endowment Policy in UAECompare whole life vs endowment insurance in UAE. Understand their differences, benefits, and choose the right plan for your financial goals.

02 Jul 2025Difference Between Whole Life and Endowment Policy in UAECompare whole life vs endowment insurance in UAE. Understand their differences, benefits, and choose the right plan for your financial goals. 23 May 2025Expat Life Insurance in UAE: Best Plans & Complete GuideExplore everything about expat life insurance in the UAE – from top plans and benefits to key reasons why expats need coverage. Secure your family's future today.

23 May 2025Expat Life Insurance in UAE: Best Plans & Complete GuideExplore everything about expat life insurance in the UAE – from top plans and benefits to key reasons why expats need coverage. Secure your family's future today. 30 Oct 2025Universal Life Insurance in UAE: Benefits and TypesDiscover the advantages of Universal Life Insurance in the UAE. Learn about flexible premiums, investment options, types of UL policies, and how to build long-term wealth and protection.

30 Oct 2025Universal Life Insurance in UAE: Benefits and TypesDiscover the advantages of Universal Life Insurance in the UAE. Learn about flexible premiums, investment options, types of UL policies, and how to build long-term wealth and protection. 15 Apr 2025Term Insurance for Women in the UAEExplore affordable term insurance for women in the UAE. Learn about benefits, best plans, eligibility, and how to choose the right coverage to protect your family.

15 Apr 2025Term Insurance for Women in the UAEExplore affordable term insurance for women in the UAE. Learn about benefits, best plans, eligibility, and how to choose the right coverage to protect your family. 15 Apr 2025Life Insurance for Parents in UAELooking to secure your parents’ financial future? Explore life insurance for parents in the UAE, including benefits, types, how to apply, and what to consider when choosing a plan.

15 Apr 2025Life Insurance for Parents in UAELooking to secure your parents’ financial future? Explore life insurance for parents in the UAE, including benefits, types, how to apply, and what to consider when choosing a plan. 28 Feb 2025Best Term Insurance Plans for Self-Employed in UAE – Secure Your FutureExplore the best term insurance plans for self-employed individuals in the UAE. Get financial security for your family & business with affordable coverage options. Compare & apply now.

28 Feb 2025Best Term Insurance Plans for Self-Employed in UAE – Secure Your FutureExplore the best term insurance plans for self-employed individuals in the UAE. Get financial security for your family & business with affordable coverage options. Compare & apply now. 28 Feb 2025Zurich Futura Whole Life Insurance – Benefits, Features & Coverage in UAEDiscover Zurich Futura Whole Life Insurance in the UAE. Get lifelong coverage, flexible benefits, and investment growth. Learn about policy features, optional riders, and how to apply today!

28 Feb 2025Zurich Futura Whole Life Insurance – Benefits, Features & Coverage in UAEDiscover Zurich Futura Whole Life Insurance in the UAE. Get lifelong coverage, flexible benefits, and investment growth. Learn about policy features, optional riders, and how to apply today! 21 Feb 2025Best Life Insurance Companies in the UAE – Compare & Choose the Right PolicyLooking for the best life insurance companies in the UAE? Compare top insurers, coverage options, and claim settlement ratios to secure your family’s financial future.

21 Feb 2025Best Life Insurance Companies in the UAE – Compare & Choose the Right PolicyLooking for the best life insurance companies in the UAE? Compare top insurers, coverage options, and claim settlement ratios to secure your family’s financial future. 19 Aug 2025Term vs Whole Life Insurance in UAE: Key Differences & BenefitsCompare term and whole life insurance in the UAE. Understand key differences, benefits, costs, and which plan suits your financial goals and budget.

19 Aug 2025Term vs Whole Life Insurance in UAE: Key Differences & BenefitsCompare term and whole life insurance in the UAE. Understand key differences, benefits, costs, and which plan suits your financial goals and budget.- 11 Feb 2025Sum Insured vs Sum Assured: Key Differences & Insurance GuideUnderstand the difference between sum insured vs sum assured in insurance. Learn about their meanings, key features, and how to choose the right coverage for your needs.

23 Jul 2024Takaful Emarat Life Insurance | Choose Best Takaful Emarat Life Insurance in UAETakaful Emarat Life Insurance UAE - Compare & Buy Takaful Emarat Life Insurance in Dubai, UAE. Get Financial assurance for your family with a Takaful Emarat Life Insurance

23 Jul 2024Takaful Emarat Life Insurance | Choose Best Takaful Emarat Life Insurance in UAETakaful Emarat Life Insurance UAE - Compare & Buy Takaful Emarat Life Insurance in Dubai, UAE. Get Financial assurance for your family with a Takaful Emarat Life Insurance 15 May 2024Why Choose Twenty Five Year Term Life Insurance?In this article, we will understand all the key details about 25 year term insurance and its usefulness.

15 May 2024Why Choose Twenty Five Year Term Life Insurance?In this article, we will understand all the key details about 25 year term insurance and its usefulness. 15 May 2024Level or Decreasing Life Insurance: What's the Difference?In this article, we will explore the distinction between decreasing vs level insurance, the benefits of each type, and how you can determine what works best for you.

15 May 2024Level or Decreasing Life Insurance: What's the Difference?In this article, we will explore the distinction between decreasing vs level insurance, the benefits of each type, and how you can determine what works best for you. 16 May 2025Level Term Life Insurance in UAE – Features and BenefitsExplore Level Term Life Insurance in the UAE – enjoy fixed premiums, guaranteed death benefits, and flexible coverage terms. Ideal for affordable long-term protection.

16 May 2025Level Term Life Insurance in UAE – Features and BenefitsExplore Level Term Life Insurance in the UAE – enjoy fixed premiums, guaranteed death benefits, and flexible coverage terms. Ideal for affordable long-term protection.- 11 Mar 202410 Crore Life Insurance Policy - A Complete GuideA 10 crore life insurance policy offers extensive coverage. It ensures the financial well-being of the family and allows them to maintain their lifestyle and meet their financial goals even in the policyholder’s absence.

23 Oct 2025Term Insurance for NRIs in UAE: Best Plans in 2026Explore top term insurance plans for NRIs in the UAE. Secure your family's future with affordable coverage tailored for expatriates. Get a quote today!

23 Oct 2025Term Insurance for NRIs in UAE: Best Plans in 2026Explore top term insurance plans for NRIs in the UAE. Secure your family's future with affordable coverage tailored for expatriates. Get a quote today!.png) 25 Apr 2025Best Life Insurance for Seniors | Protect Your FutureExplore affordable life insurance for seniors. Compare plans, get a quote, and find the best coverage for your needs. Start securing your future today!

25 Apr 2025Best Life Insurance for Seniors | Protect Your FutureExplore affordable life insurance for seniors. Compare plans, get a quote, and find the best coverage for your needs. Start securing your future today! 07 Aug 20231 Crore Term Insurance Plans In India: Here’s What You Need to Know!1 Crore Term Insurance Plans - Term insurance, a type of life insurance providing coverage for a specified tenure, offers a cost-effective way for individuals to financially protect their loved ones in the event of an unexpected death.

07 Aug 20231 Crore Term Insurance Plans In India: Here’s What You Need to Know!1 Crore Term Insurance Plans - Term insurance, a type of life insurance providing coverage for a specified tenure, offers a cost-effective way for individuals to financially protect their loved ones in the event of an unexpected death. 06 Dec 2024Life Insurance for Couples : Everything You Need to KnowMake sure your loved ones are taken care of – get life insurance for couples today! Explore the significance of life insurance for married couples and how it can provide a safety net for the family's financial well-being.

06 Dec 2024Life Insurance for Couples : Everything You Need to KnowMake sure your loved ones are taken care of – get life insurance for couples today! Explore the significance of life insurance for married couples and how it can provide a safety net for the family's financial well-being. 02 Aug 2023Understanding Life Insurance for 60 Year OldsLife insurance for senior citizens over 60 years numerous life insurance plans for coverage related to death, critical illnesses, situations where one is unable to work due to disabilities, and more.

02 Aug 2023Understanding Life Insurance for 60 Year OldsLife insurance for senior citizens over 60 years numerous life insurance plans for coverage related to death, critical illnesses, situations where one is unable to work due to disabilities, and more. 07 Aug 2023Term Life Insurance with Critical Illness CoverCritical illness covers a variety of illnesses, so be sure to find the right policy for you and your family. Check out our selection of term life insurance with critical illness cover today!

07 Aug 2023Term Life Insurance with Critical Illness CoverCritical illness covers a variety of illnesses, so be sure to find the right policy for you and your family. Check out our selection of term life insurance with critical illness cover today! 05 Sep 2023Your Ultimate Guide to Life Insurance Corporation of IndiaLife Insurance Corporation of India - LIC aims to serve as a comprehensive guide for all those interested in learning more about LIC of India, delving into the core aspects of the corporation, its offerings, and its impact on the lives of millions of Indians.

05 Sep 2023Your Ultimate Guide to Life Insurance Corporation of IndiaLife Insurance Corporation of India - LIC aims to serve as a comprehensive guide for all those interested in learning more about LIC of India, delving into the core aspects of the corporation, its offerings, and its impact on the lives of millions of Indians.- 23 Sep 2025Defining Spouse Term Insurance: Term Insurance for Husband and WifeWe will cover couple term insurance, discussing its importance, key features, benefits, and factors to consider when choosing a plan.

24 Jun 2025Best Term Insurance Plan in India 2026Term insurance presents an economical way to secure one's family's financial future and have cover for their financial obligations such as mortgage payments, education expenses, and daily living costs.

24 Jun 2025Best Term Insurance Plan in India 2026Term insurance presents an economical way to secure one's family's financial future and have cover for their financial obligations such as mortgage payments, education expenses, and daily living costs. 07 Aug 2023Life Insurance for 65 and Older - Benefits & TipsCheck out our top picks for 65+ life insurance plans! Learn more about the benefits of life insurance for those over 65 years old in this post.

07 Aug 2023Life Insurance for 65 and Older - Benefits & TipsCheck out our top picks for 65+ life insurance plans! Learn more about the benefits of life insurance for those over 65 years old in this post. 19 Sep 2025LIC Term Insurance 1 Crore – An OverviewWe will take a closer look at LIC term insurance 1 crore and cover all its related aspects.

19 Sep 2025LIC Term Insurance 1 Crore – An OverviewWe will take a closer look at LIC term insurance 1 crore and cover all its related aspects.- 09 Dec 2025Term Insurance Premium Calculator - A Complete GuideTerm insurance premium calculator in the UAE offers numerous advantages, streamlining the process of selecting the most suitable term insurance plan.

07 Aug 2023Life Insurance for Seniors over 70 Years - Benefits & TipsDon't wait until it's too late to get life insurance for seniors. Here are everything you need to know about getting life insurance for seniors over 70 years of age.

07 Aug 2023Life Insurance for Seniors over 70 Years - Benefits & TipsDon't wait until it's too late to get life insurance for seniors. Here are everything you need to know about getting life insurance for seniors over 70 years of age. 07 Aug 2023The Best Life Insurance Cover in the UAE - Securing Your Loved Ones' FutureLife Insurance Cover in UAE - We will show you the different types of life insurance available in the UAE and which is best for you.

07 Aug 2023The Best Life Insurance Cover in the UAE - Securing Your Loved Ones' FutureLife Insurance Cover in UAE - We will show you the different types of life insurance available in the UAE and which is best for you.- 06 Nov 2023Can You Have Two Life Insurance Policies?This article delves deep into the realm of holding multiple term insurance policies, highlighting the benefits and answering your pressing queries regarding this facet of financial planning.

02 Aug 2023Best 5 crore term life insurance: Best Term Plans in UAEWe will discuss 5 crore term life insurance in detail, whether it is suitable for you and your family, and other factors to keep in mind.

02 Aug 2023Best 5 crore term life insurance: Best Term Plans in UAEWe will discuss 5 crore term life insurance in detail, whether it is suitable for you and your family, and other factors to keep in mind. 02 Aug 2023Life Insurance For People Over 50 : Plans & BenefitsLife insurance also allows seniors to leave a legacy for their beneficiaries, offering a means to support their families or contribute to charitable causes.

02 Aug 2023Life Insurance For People Over 50 : Plans & BenefitsLife insurance also allows seniors to leave a legacy for their beneficiaries, offering a means to support their families or contribute to charitable causes. 30 Oct 2025How Many Types of Life Insurance Policies in UAEThere are different type fo policies in market like whole life, child life, and endowment life insurance policies, we intend to illuminate the unique characteristics and benefits of each type.

30 Oct 2025How Many Types of Life Insurance Policies in UAEThere are different type fo policies in market like whole life, child life, and endowment life insurance policies, we intend to illuminate the unique characteristics and benefits of each type. 03 Jan 2024Life Insurance for Young Adults - Securing Your Tomorrow, Today!We will explore the significance of life insurance for young adults, the various options available, and why it's a wise decision to secure your future today.

03 Jan 2024Life Insurance for Young Adults - Securing Your Tomorrow, Today!We will explore the significance of life insurance for young adults, the various options available, and why it's a wise decision to secure your future today.- 07 Aug 2023Best Life Insurance for Seniors Over 75 in UAEExplore the importance of life insurance for seniors over 75, discuss the benefits it offers, and provide guidance on choosing the right policy. Get started today and find the best policy for you and your family!